I have been investing for 10 years now and over that time I’ve seen and used some pretty exciting property investing strategies. So it now takes a lot to get me excited and this strategy has got me very excited!

Sure you can do some pretty creative and profitable things developing property but usually the money required and risk involved keeps the average person on the sidelines.

About 3 months ago I came across the idea of dual income property and I must say I got very excited by the super high rental returns of 6% to 7.5% yield which can be achieved here in Perth.

The more I looked into dual income property the more excited I got and now I am convinced that it’s a strategy every investor should use as part of their portfolio, when holding property for the long term… Here are all the ins and outs.

Queensland investors have known about it for years!

I was speaking to a well known Perth builder telling him that I was mainly interested in properties that gave a good cash flow. Which was when he told me about their dual income designs which they have been building for eastern states investors.

I was speaking to a well known Perth builder telling him that I was mainly interested in properties that gave a good cash flow. Which was when he told me about their dual income designs which they have been building for eastern states investors.

After doing a bit more research I found that dual income property has been very popular in QLD for years.

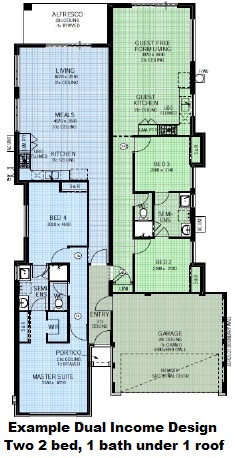

The design comprises two independent, separately rentable dwellings under the one roof on a typical block size of 350-450sqm. I had never heard of it being done here in Perth, so I just had to get more information. It turns out there is quite a lot involved in getting the design to be practical and meet council approvals, luckily they had already spent a lot of time working all these things out.

What do the numbers look like?

The typical rental property in the outer suburbs of Perth is now fetching a 5.0% rental yield. So for example you could build a standard 4 bedroom, 2 bathroom house in Caversham for $520,000 which would likely rent for $490-$500pw.

A dual income house costs about an extra $80,000 to $100,000 to build (depending on design) and we are finding that they are renting for 6-6.5% rental yield. So for example you could build a dual income property with two separate 2 bedroom, 1 bathroom dwellings under the one roof for $595,000 which would rent for $360pw each for a total rent of $720pw.

This is a great rental return for residential property and the best part is that you don’t have to go to areas of greater risk that you may not be comfortable with. These can be built in the Perth metro area… not country towns, mining towns or interstate.

Strong rental demand expected

In most new estates there is virtually nothing for singles and couples to rent at this lower price, so you should have no trouble finding tenants. At present the only option for them is a 3 bedroom, 2 bathroom villa, which in Caversham for example are typically renting for $440pw.

Taking it further with dual income apartments

Only a month ago, I was speaking to a successful developer here in Perth about dual income designs and they were working on the same principle being applied to an apartment. Of course! All we are talking about is having two separate rentable spaces on the one strata title, why didn’t I think of that?

Only a month ago, I was speaking to a successful developer here in Perth about dual income designs and they were working on the same principle being applied to an apartment. Of course! All we are talking about is having two separate rentable spaces on the one strata title, why didn’t I think of that?

Their project is in Coolbellup in a great location handy to Fiona Stanley hospital and Murdoch university. The project is only just being released now, which I am lucky enough to be marketing. Prices are starting at $477,750 for a dual key apartment with two separate 1 bedroom, 1 bathroom dwellings, with a combined expected rental return of $700pw… that is a whopping rental yield of 7.6%.

If that doesn’t get you excited, I don’t know what will!

Why negative gearing is a bad idea if you can avoid it

Each month many investors still come to me wanting to reduce their tax with negative gearing. They don’t understand that by negative gearing you are getting a tax break for losing money on your rental property. The government allows you to claim back 30-50 cents on every dollar you lose but it still means you are losing money. And there is plenty of talk that negative gearing is up for review at the moment by the current government. So don’t count on it and certainly don’t seek it out.

Depreciation is the best way to save on tax

The best way to save on tax is by buying a new property, so you benefit from having a high depreciation from new fixtures, fittings, plant, equipment and the building to write off. This can give you a reduction by as much as $15,000-$25,000 in your taxable income. Plus because it’s a paper loss, it doesn’t cost anything out of your pocket and will greatly improve your cash flow.

Naturally, with a dual income property having a higher build cost, there is even more to depreciate for greater tax savings.

You never go broke making a profit

I love this saying! The whole reason we invest in property is to grow our capital and replace our income. So if you can still receive the same capital growth, why wouldn’t you also get a better rental return as well? It means that you are one step closer to replacing your income or having more for other investments.

Insulation against interest rate rises

One of the other major benefits of dual income property is protection against future rises in interest rates. We are at historically low rates at the moment so it’s only a matter of time before they go up again. With the extra rental return you have a healthy buffer on potential future rises.

Protection against vacancy

There is nothing that hurts us investors more than having a vacant property! We do everything possible to ensure minimum vacancy between tenants but with a dual income property you can arrange your leases to expire in different months. That way if one tenant decides to move out, you have still got an income from the other one.

What about re-sale value?

Whenever you solve a problem you can expect it to have a strong re-sale value in the market. This type of housing doesn’t only provide a great rental return for investors, it also provides more affordable living options for families or independents purchasing together. I know many extended families that would love the idea of living close by without sharing the same physical space.

How much money do I need to get started?

It definitely pays to speak to a knowledgeable finance broker who can help you make the most of your savings and equity. The rule of thumb is that you will require at least $50,000 in savings or equity to fund your deposit and stamp duty and be able to borrow at least $420,000 for these types of property.

Maximising growth with dual income

You can probably tell by now that I am very excited about dual income property.

So much so that I have spent the last 3 months working with some of Perth’s most respected builders to put together complete turn key, house and land packages in the land estates across Perth that I think have the best potential for capital growth. I have done lots of research to find the areas that are both very popular with home buyers, which also have lots of infrastructure going in to further boost demand to the area.

Plus I also have those dual income apartments in Coolbellup, which I mentioned above. With the location being so handy to Fiona Stanley hospital and Murdoch university, and a super impressive expected rental yield of 7.4%, it really is a no brainer.

So if you want the best of both worlds- growth potential and cash flow, get in touch for more info on these extremely unique dual income designs.

Tell me what you think below

I’d love to also hear what you think of dual income property, so let me know below.

Have you got any questions?… post them below or get in touch.

This is a good and clever concept Jarrad. it has been used in Europe for a very long time. They are called semi-detached houses. We used to live in one such house and it was quite a large one too.

And we recently sold 2 2×1 duplex in waterford on the same principle. they have been around for a long time Jarrod.

Hi Sushila, you are right… Duplex’s where built in the 1960’s and 1970’s to provide a better return for investors and are the same concept of building under the one roof 🙂

But they are a very different property type. The typical duplex is on much larger land of 800sqm+ and each has a separate strata title so they can be sold individually.

These properties can be held in your Self-Managed Superfund. Rent is taken into account when the bank considers how much they can lend you so higher yield allows higher borrowing.

Do you know that you can add a Granny Flat to an existing property in a SMSF and significantly increase the yield/return!

Sondergaard Accountants are SMSF and Property Specialists. Any questions email Gina Davidson, our SMSF Specialist on [email protected].

Hi Charles, my understanding is that you can’t borrow to build a house on land or borrow to build a granny flat in a SMSF. So the only way you can do that is if you have the cash in super to build them without borrowing.

You can borrow to buy an Off the Plan property in a SMSF, like the Coolbellup apartments I mentioned, where you are settling the apartment when it is complete.

Is this correct?… Thanks for your input!

Hi Jarrad,

Have you noted any issues in getting the building approvals? Because it’s like building 2 houses on one block of land.

Hi Victor, the 2 builders I am working with are full bottle on the approvals side so not having any problems there. The main requirements are for it to be under one main roof and have the common entry.

Hi Jarrad

We just completed 2 dual occupancy dwellings. They both don’t have common entry: one in the front and one on the side for privacy and no issues for approval.

Both have separate aircon and a sub meter to divide the power consumption.

Water and gas dividing to 2 separate tenants is an unknown area.

Currently divided per person living in the house, but as per REIWA a very grey area.

The Water corporation is not providing 2 water meters on the same title, same with gas.

How would you recommend to divide water and gas bills?

Hi Didi,

You would either need make those services included in the rent and put them under your name, charging extra rent to offset them…

Or include in the lease an agreement to apportion the cost of those services in accordance with the number of tenants living in each.